According to IMARC Group's report titled "India Fintech Market Size, Share, Trends and Forecast by Deployment Mode, Technology, Application, End User, and Region, 2026-2034", The report offers a comprehensive analysis of the industry, including market share, trends, forecast, growth and regional insights.

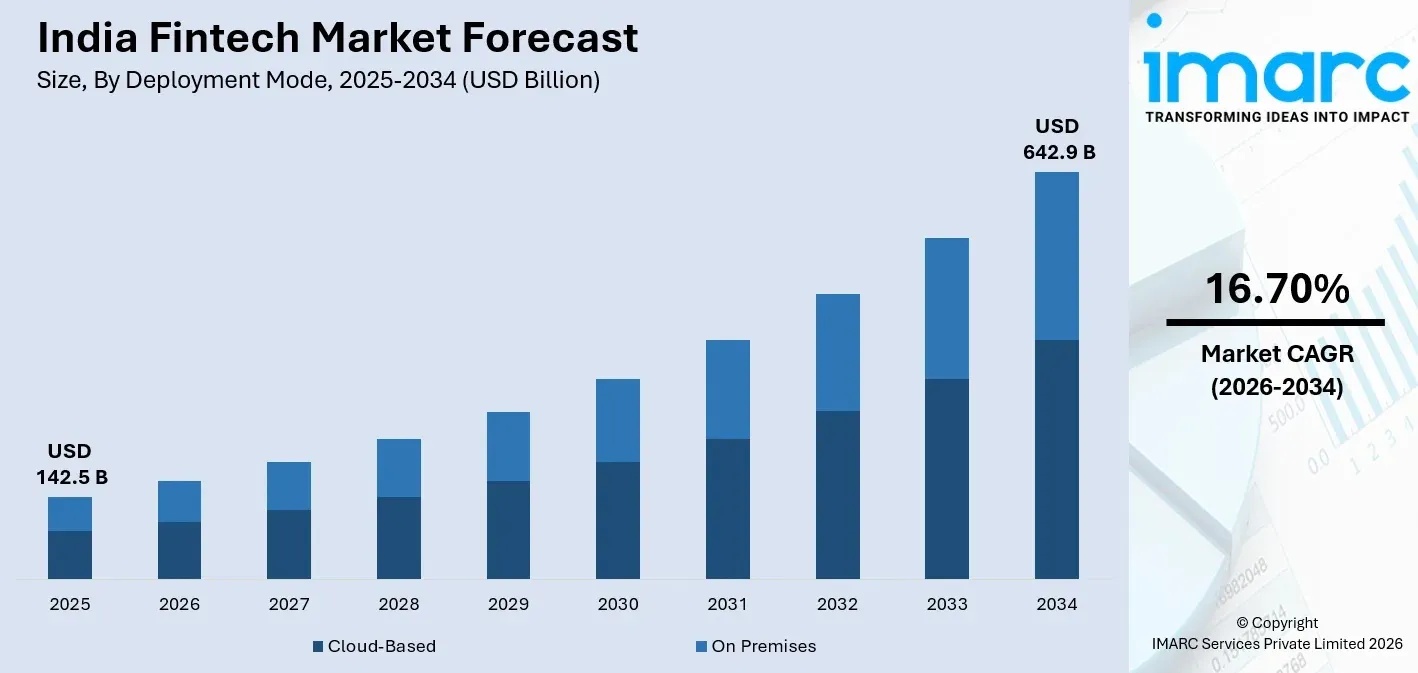

The India Fintech market size, valued at USD 142.5 Billion in 2025, is projected to reach USD 642.9 Billion by 2034, growing at a CAGR of 16.70% from 2026-2034.

India’s financial services sector is undergoing a comprehensive structural formalization, driven by a world-leading Digital Public Infrastructure (DPI) that has successfully decoupled high-frequency transactional banking from physical branch constraints. As regulatory frameworks mature and corporate digital adoption deepens, the domestic financial technology ecosystem presents highly predictable, asset-light entry points for private equity and institutional investors looking to scale high-yield capital deployment.

- Massive Digital Market Scale: Capital deployment into the sovereign fintech ecosystem taps into a market valued at USD 142.5 Billion in 2025, which is structurally positioned for long-term expansion due to a deep shift toward digital-first financial behavior.

- Dominance of Transactional Architecture: Focusing investment on payment and fund transfer applications captures the largest segment of the ecosystem, commanding a dominant 46.5% market share driven by the deep integration of mobile wallets and real-time merchant networks.

- Enterprise Infrastructure Integration: Strategic positioning within core banking end-user systems allows enterprise software providers to secure steady, long-term software-as-a-service (SaaS) revenues, as traditional commercial banking institutions capture a 41.8% market share by modernizing their legacy digital rails.

- Technological Modernization Execution: Expanding business operations into Application Programming Interface (API)-driven open banking architectures captures the leading technology segment at a 27.9% market share, enabling frictionless digital lending, embedded finance, and automated underwriting tools.

The Strategic Market Challenge: Navigating the Fintech Market in India

The primary structural bottleneck within India's tech-driven financial services framework lies in the complex compliance-innovation paradox, where agile market participants struggle to align rapid user acquisition with the central bank’s tightening data-sovereignty and digital lending mandates. Enterprise executives frequently overlook the escalating operational burden of recurring compliance audits and the financial pressures of rising customer acquisition costs within highly saturated urban demographics. Consequently, mitigating this structural friction by migrating from speculative customer-acquisition models to high-governance, compliance-first infrastructure is imperative for protecting long-term enterprise valuations and avoiding sudden operational interruptions.

➤ Access Key Market Statistics and Actionable Insights - Request Sample Report: https://www.imarcgroup.com/india-fintech-market/requestsample

India's Strategic Vision for the Fintech Market:

-

Sovereign Network Globalization: Expanding the international footprint of the India Stack through bilateral cross-border payment linkages, establishing the Unified Payments Interface (UPI) as a global benchmark for real-time retail settlements.

-

Complete Financial Formalization: Utilizing alternative data architectures to extend formal credit, low-cost micro-insurance, and automated personal wealth management tools to previously underserved tier-2 and tier-3 rural consumer demographics.

-

Digital Public Infrastructure Scalability: Upgrading underlying technological layers via secure open-source APIs to allow traditional banking systems and third-party applications to interact smoothly without operational friction.

Why Invest in the India Fintech Market: Key Growth Drivers & ROI

-

Sovereign Infrastructure Tailwinds: Massive public deployment of the Jan Dhan-Aadhaar-Mobile (JAM) trinity establishes an immediate, zero-friction consumer onboarding funnel, lowering structural identity verification costs for private financial institutions.

-

Exponential Mobile Consumption Volumes: Pervasive national access to low-cost wireless data networks and affordable smartphone devices creates continuous consumer engagement, ensuring high daily active user metrics across transactional platforms.

-

Open Banking API Proliferation: The structural expansion of secure, real-time data-sharing networks allows non-banking financial companies (NBFCs) to deploy custom digital lending instruments, addressing the substantial capital credit gap within the domestic MSME sector.

-

Institutional Risk Automation: Integrating intelligent analytics and automated credit scoring engines directly lowers credit default rates, delivering predictable, optimized return on investment (ROI) metrics for corporate underwriting portfolios.

India Fintech Market Trends & Future Outlook:

-

Pivoting to Cloud-Native Architecture: Accelerated migration toward scalable, cloud-based deployment models, which capture a leading 64.7% market share by offering rapid product development cycles and lower capital expenditure barriers.

-

Geographic Expansion Into Central Corridors: Geographically shifting operational focus toward West and Central India to tap into its dominant 34.6% regional market share, anchored by primary financial corporate headquarters and digitized manufacturing zones.

-

Biometric Payment Modernization: Fleet migration of retail transactional channels toward PIN-less authentication frameworks, utilizing advanced facial recognition and fingerprint data to reduce point-of-sale friction.

-

Alternative B2B Credit Integration: The systematic embedding of buy-now-pay-later (BNPL) mechanisms and structured working-capital lines directly into business-to-business supply chain checkout flows to capture steady, high-margin transaction volumes.

Regulatory Landscape & Policy Catalysts in India:

-

RBI Digital Lending Guidelines: The Reserve Bank of India (RBI) enforces strict rules on fund flows and co-lending arrangements, restricting unbacked credit syndication and driving corporate focus toward sustainable balance-sheet lending.

-

First Loss Default Guarantee (FLDG) Frameworks: According to the Reserve Bank of India, formalized FLDG frameworks permit regulated entities to accept structured credit loss guarantees from technology partners up to a capped 5% threshold, de-risking co-lending partnerships.

-

Digital Personal Data Protection (DPDP) Act Compliance: Rigid data-privacy mandates established under national legislative acts compel technology firms to deploy localized data storage architectures, establishing consumer consent as a baseline operational requirement.

-

Zero MDR Policies on Public Infrastructure: State-directed mandates removing merchant discount rates (MDR) for foundational payment mechanisms accelerate grassroots retail merchant onboarding, providing technology operators with a massive, data-rich pool for cross-selling financial services.

-

RBI Innovation Hub System Deployment: Centralized support via dedicated regulatory sandboxes accelerates the domestic testing of advanced anti-fraud tools, allowing institutions to identify unauthorized accounts before material financial losses occur.

➤ Explore the Exact Chapters and Data Scope - Get Full Brochure: https://www.imarcgroup.com/request?type=report&id=10442&flag=A

By the IMARC Group, the Top Competitive Landscape & their Positioning:

- PhonePe (Walmart Inc.)

- Google Pay (Alphabet Inc.)

- Paytm (One97 Communications Ltd.)

- Razorpay

India Fintech Market Segmentation:

The market report offers a comprehensive analysis of the segments, highlighting those with the largest India fintech market share. It includes forecasts for the period 2026-2034 and historical data from 2020-2025 for the following segments.

Deployment Mode Insights

- Cloud-Based (64.7% market share in 2025)

- On Premises

Technology Insights

- Application Programming Interface (27.9% majority share in 2025)

- Artificial Intelligence

- Blockchain

- Robotic Process Automation

- Data Analytics

- Others

Application Insights

- Payment and Fund Transfer (46.5% share in 2025)

- Loans

- Insurance and Personal Finance

- Wealth Management

- Others

End User Insights

- Banking (41.8% market share in 2025)

- Insurance

- Securities

- Others

Regional Insights

- West and Central India (34.6% market share in 2025)

- North India

- South India

- East India

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

➤ Shape the Data to Answer Your Specific Questions - Request Customization: https://www.imarcgroup.com/request?type=report&id=10442&flag=E

Frequently Asked Questions (FAQs)

Q1: What is the current value and projected growth of the India Fintech Market?

According to IMARC Group, the India fintech market was valued at USD 142.5 Billion in 2025 and is projected to reach USD 642.9 Billion by 2034, exhibiting a CAGR of 16.70% during the 2026–2034 forecast period.

Q2: Which deployment mode commands the highest market share?

The cloud-based deployment model holds the primary market share at 64.7% in 2025, driven by the operational necessity for fintech platforms to leverage auto-scaling, reduce server downtime, and host agile API connections.

Q3: How is the integration of APIs shaping the domestic technology layer?

Application Programming Interfaces (APIs) represent the leading technology segment with a 27.9% market share, acting as the primary digital conduit that enables independent fintech systems to link seamlessly with legacy commercial bank ledgers.

Q4: What specific application sector drives absolute transaction velocity?

The payment and fund transfer vertical commands the leading application share at 46.5%, anchored heavily by the mass institutionalization of UPI and real-time electronic ledger settlements across both retail and corporate business networks.

Q5: What represents the largest growth segment for alternative capital providers?

Digital lending tech is currently the highest-margin investment segment, targeting the significant USD 300 Billion credit gap present within the underbanked MSME sector through the deployment of short-term supply chain financing.

Strategic Insight & Verdict:

India’s financial technology environment is executing a clear migration from a payment facilitation utility to a heavily formalized credit, wealth, and embedded banking infrastructure. Analyzing this maturation across the technological matrix, we at IMARC Group have observed that long-term asset growth relies strictly on optimizing API-driven co-lending platforms and establishing deep regulatory compliance. For global investors and corporate strategists, the optimal path requires immediate capital allocation toward data-compliant micro-lending and B2B enterprise software platforms to lock in premium margins within this expanding USD 642.9 Billion market.

Gaurav, Digital Market Research Strategist at IMARC Group: https://www.linkedin.com/in/gourav-shah-005425345

Verified Data Source: IMARC Group

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel NoD) +91 120 433 0800

United States: +1-202071-6302

Comments (0)