According to IMARC Group's report titled "India Life Insurance Market Size, Share, Trends and Forecast by Type, Premium Type, Premium Range, Provider, Mode of Purchase, and Region, 2026-2034", The report offers a comprehensive analysis of the industry, including India life insurance market forecast, growth and regional insights.

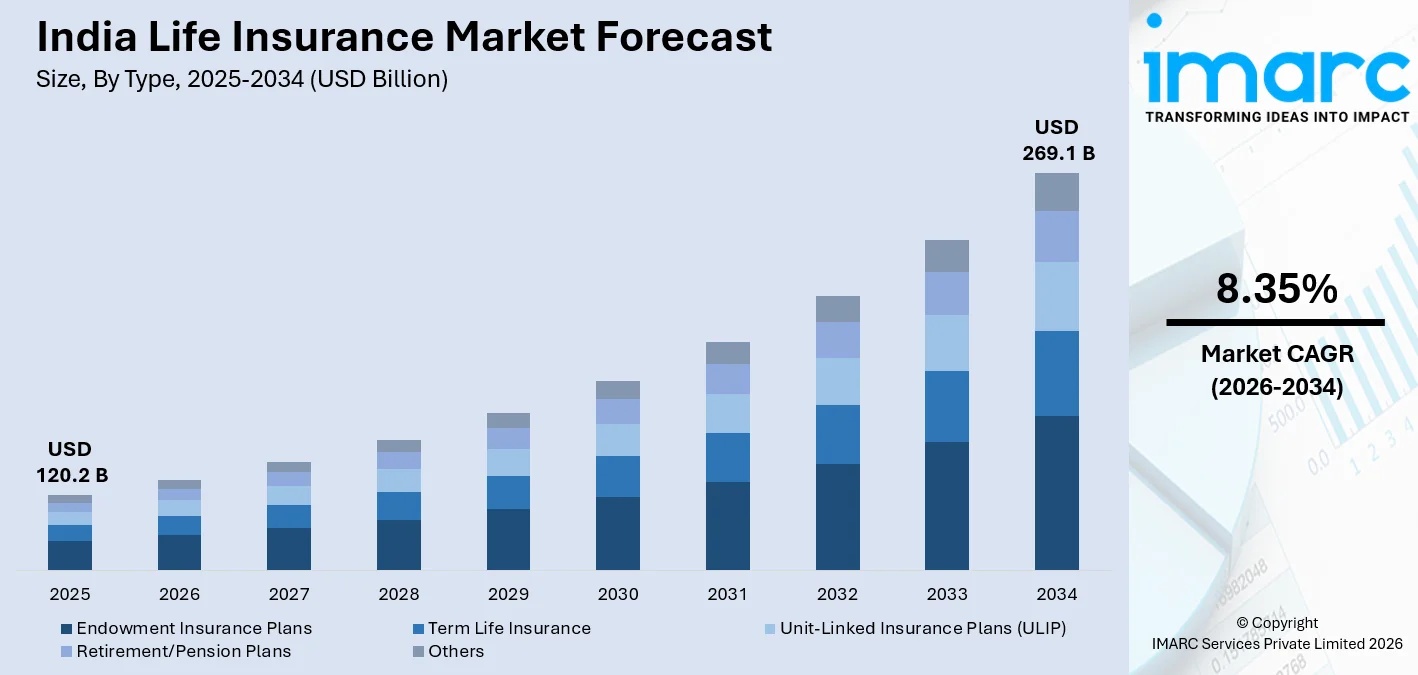

India life insurance market size stood at USD 120.2 Billion in 2025, and it is expected to reach USD 269.1 Billion by 2034, with a compound annual growth rate of 8.35% during 2026-2034.

India's financial services ecosystem is executing a massive structural expansion, with the life insurance sector evolving from a traditional tax-saving instrument into a digitally integrated, comprehensive wealth accumulation and protection grid.

• Demographic Catalyst: A surging middle class and increasing financial literacy are driving robust demand for pure protection term plans and Unit-Linked Insurance Plans (ULIPs).

• Digital Distribution: Insurtech platforms and bancassurance channels are fundamentally reshaping market access, significantly lowering customer acquisition costs across Tier-2 and Tier-3 urban clusters.

The Strategic Market Challenge: Navigating the Life Insurance Market in India

A persistent structural bottleneck within the BFSI sector is the high concentration of distribution networks in major metropolitan centers, leading to a severe protection deficit in rural demographics. Leaders frequently overlook the friction caused by complex underwriting protocols and the lack of hyper-personalized, "bite-sized" products tailored for India's massive informal economy. This operational gap inflates policy lapsation rates, restricts scalable penetration, and severely limits the long-term embedded value (EV) of legacy portfolios, preventing national insurance density from achieving global parity.

➤ Access Key Market Statistics and Actionable Insights - Request Sample Report: https://www.imarcgroup.com/india-life-insurance-market/requestsample

India's Strategic Vision for the Life Insurance Market

• Insurance for All by 2047: Spearheaded by national regulatory authorities, the primary macroeconomic objective is to achieve universal life insurance coverage by heavily utilizing Digital Public Infrastructure (DPI) to democratize access.

• Risk-Based Capital (RBC) Regime Transition: Government and regulatory shifts are focused on transitioning from a factor-based solvency regime to an RBC framework, optimizing capital allocation and enabling insurers to price granular mortality risks accurately.

• State-Level Penetration Targets: The implementation of the State Insurance Plan ensures localized distribution architectures, aiming to drastically improve rural insurance density by integrating awareness campaigns directly at the gram panchayat and district levels.

Why Invest in the India Life Insurance Market: Key Growth Drivers & ROI

• Insurtech and Open Architecture Integration: Capitalizing on centralized digital marketplaces effectively eliminates intermediary friction. Investing in digital-first distribution networks yields immediate ROI through vastly reduced commission overheads, accelerated policy issuance, and improved operational margins.

• Financialization of Domestic Savings: As the urban demographic shifts capital from physical assets to financial markets, allocating resources toward hybrid investment-insurance products like ULIPs captures a massive cohort seeking dual-benefit wealth creation and tax-efficient returns.

• Hyper-Personalization via AI: Deploying AI-driven underwriting models allows insurers to precisely price risk based on granular lifestyle and biometric data. This technological upgrade structurally reduces claim repudiation rates, mitigates adverse selection, and optimizes the overall profitability of the risk pool.

India Life Insurance Market Trends & Future Outlook

• Micro-Insurance Proliferation: There is a definitive trajectory toward sachet-sized, low-ticket policies designed specifically to capture massive volume within the uninsured gig economy and rural sectors.

• Omnichannel Bancassurance Expansion: Banking institutions are aggressively integrating life insurance offerings directly into their mobile banking applications, ensuring highly efficient, point-of-sale policy conversions.

• Embedded Insurance Ecosystems: Non-financial platforms (e-commerce, travel, fintech) are increasingly embedding contextual term cover at the digital checkout phase to drive instantaneous, high-frequency adoption.

• Transition to Preventive Wellness: Insurers are evolving from passive risk-payers to active health partners, offering dynamic premium discounts linked to verifiable wellness data gathered via wearable IoT devices.

Regulatory Landscape & Policy Catalysts in India

• Bima Sugam Deployment: According to the Insurance Regulatory and Development Authority of India (IRDAI), the deployment of this centralized electronic marketplace legally mandates a unified infrastructure for policy purchase, servicing, and claim settlement.

• E-Insurance Account (eIA) Mandate: As enforced by the IRDAI, the compulsory dematerialization of all new insurance policies into electronic accounts ensures absolute data integrity, prevents fraudulent issuance, and lowers administrative costs.

• Enhanced Surrender Value Norms: According to the IRDAI, revised guidelines on surrender values strictly protect policyholders from heavy penal deductions, structurally forcing insurers to redesign product architectures to prioritize long-term retention.

• FDI Limit Enhancement: According to the Ministry of Finance, elevating the Foreign Direct Investment (FDI) limit to 74% under the automatic route acts as a profound catalyst for cross-border joint ventures, injecting critical institutional capital into domestic firms.

• Open Architecture in Bancassurance: Regulatory frameworks explicitly prohibit exclusive distribution tie-ups, legally allowing banking institutions to partner with multiple life insurers to prevent market monopolization and increase consumer choice.

➤ Explore the Exact Chapters and Data Scope - Get Full Brochure: https://www.imarcgroup.com/request?type=report&id=32518&flag=A

By the IMARC Group, the Top Competitive Landscape & their Positioning:

• Life Insurance Corporation of India

• HDFC Life Insurance

• SBI Life Insurance

India Life Insurance Market Segmentation:

The market report offers a comprehensive analysis of the segments, highlighting those with the largest India life insurance market share. It includes forecasts for the period 2026-2034 and historical data from 2020-2025 for the following segments.

Type Insights

• Endowment Insurance Plans (36.7% market share in 2025)

• Term Life Insurance

• Unit-Linked Insurance Plans (ULIP)

• Retirement/Pension Plans

• Others

Premium Type Insights

• Regular (68.4% share in 2025)

• Single

Premium Range Insights

• Medium (44.2% market share in 2025)

• Low

• High

Provider Insights

• Insurance Companies (62.5% market share in 2025)

• Insurance Agents/Brokers

• Others

Mode of Purchase Insights

• Offline (71.3% majority share in 2025)

• Online

Regional Insights

• South India (33.8% share in 2025)

• North India

• West India

• East India

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

➤ Shape the Data to Answer Your Specific Questions - Request Customization: https://www.imarcgroup.com/request?type=report&id=32518&flag=E

Frequently Asked Questions (FAQs)

1. What is the current value and projected growth of the India Life Insurance Market?

According to IMARC Group, the India life insurance market reached a value of USD 120.2 Billion in 2025 and is projected to reach USD 269.1 Billion by 2034, exhibiting a CAGR of 8.35% during the forecast period.

2. What is the primary factor driving the demand for term insurance?

The heightened awareness of financial security and mortality risk, coupled with the systemic under-penetration of pure protection plans, is driving aggressive volume growth in the term insurance segment among the urban middle class.

3. How is the distribution landscape evolving?

While agency channels historically dominated, the market is executing a massive structural shift toward bancassurance and direct-to-consumer (D2C) digital aggregators to bypass traditional intermediary costs and capture a younger demographic.

4. What role does Bima Sugam play in the market?

Bima Sugam functions as a unified digital public infrastructure, effectively operating as an electronic marketplace that democratizes access, reduces administrative friction, and structurally lowers overall premium costs for the end-consumer.

5. How are private players competing with public sector entities?

Private insurers are aggressively capturing market share by focusing on affluent urban demographics, deploying superior digital user interfaces, and offering highly customized, high-margin Unit-Linked Insurance Plans (ULIPs).

Strategic Insight & Verdict:

The Indian life insurance sector is executing a definitive pivot from a push-based distribution model to a digitally integrated, pull-driven financial utility. Analyzing this regulatory and technological modernization, we at IMARC Group have observed that long-term profitability is strictly tied to dominating the digital distribution infrastructure and mastering AI-driven underwriting. For corporate investors and CXOs, the strategic mandate is absolute: deploy capital into insurtech architectures, bancassurance partnerships, and sachet-sized product engineering to capture exponential yields in this rapidly expanding USD 248.37 Billion ecosystem.

Gaurav, Digital Market Research Strategist at IMARC Group: https://www.linkedin.com/in/gourav-shah-005425345

Verified Data Source: IMARC Group

About us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services.

IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel NoD) +91 120 433 0800

United States: +1-202071-6302

Comments (0)